Initial Disclosure Document Guide

December 2024 // Version 3.0

Overview

This is an example layout for an Initial Disclosure Document (IDD), with guidance on the content you should include under each section. It is your responsibility to ensure the information you include follows the requirements set out by the Financial Conduct Authority.

There are several disclosures that must be given to the customer prominently and in good time before they proceed with the application. An IDD is a clear, concise, and compliant way of providing this information, and should be written in a way that it is easily understood by the customer.

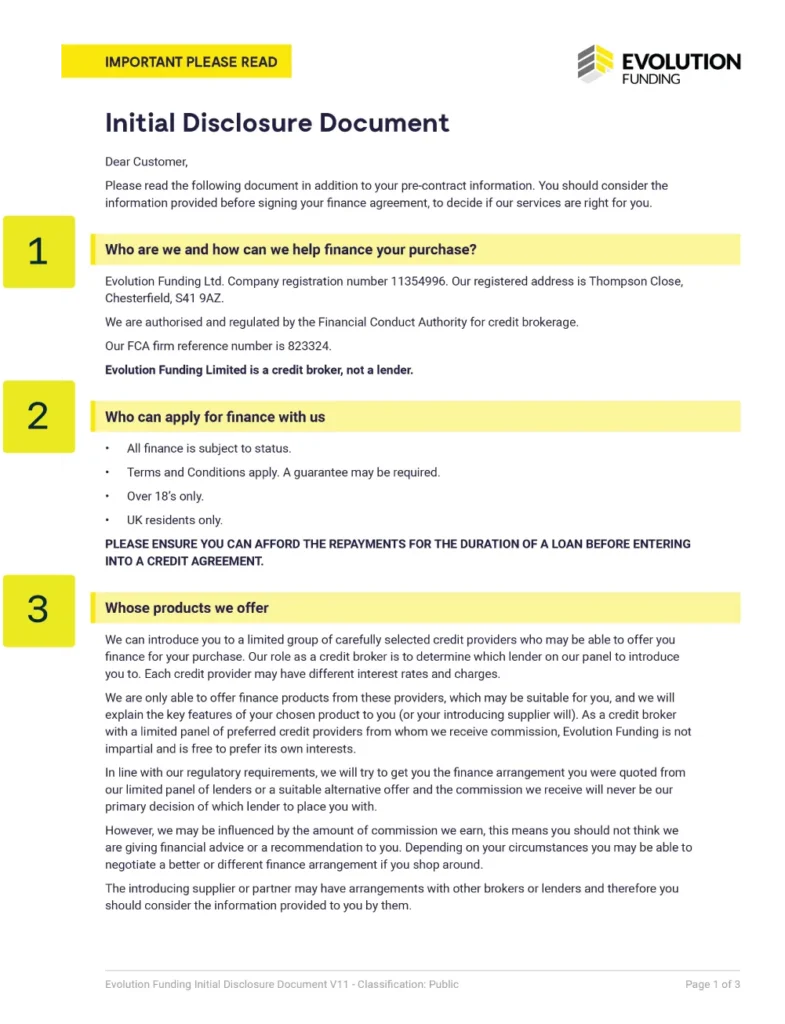

1. Company information and regulatory status

- Legal name.

- Company registration number.

- Registered address.

- Your FCA status disclosure.

- If you are an Appointed Representative of a Principal firm, then you should state this.

- Your FCA firm reference number.

- You should also state that you act as a credit broker and not a lender.

2. Who can apply for finance with us?

Any eligibility criteria, such as:

- Finance is subject to status.

- Terms and Conditions apply.

- A guarantee may be required.

- Over 18s only.

- UK residents only.

- PLEASE ENSURE YOU CAN AFFORD THE REPAYMENTS FOR THE DURATION OF A LOAN BEFORE ENTERING INTO A CREDIT AGREEMENT.

3. Whose products we offer

- Are there any limitations in your panel? Are you working exclusively with one or more lenders or are you independent?

- If you are a franchised retailer who has an arrangement with a captive lender you may choose to mention them by name and explain your process to introduce customers to that lender first.

- Are there any differences between the providers on your panel? For example, each credit provider may have different interest rates and charges (this can be included just in general terms).

- If you charge any fees for arranging the finance.

- Whether you offer independent financial advice.

- If you do or don’t give any advice or recommendations to customers.

- If you don’t offer advice, you should explain:

- you are acting as a credit broker but are not impartial and that you may act in your own commercial interests.

- you are not providing independent financial advice.

- no advice or recommendations will be given to the customer, and that they may be able to get a better deal elsewhere.

- In line with regulatory requirements, you should explain that you will try to get the customer the finance arrangement they were quoted from your limited panel of lenders or a suitable alternative offer.

- Explain that the commission you receive will never be your primary decision of which lender to place the customer with, if that is right for you (this is in line with FCA CONC rules).

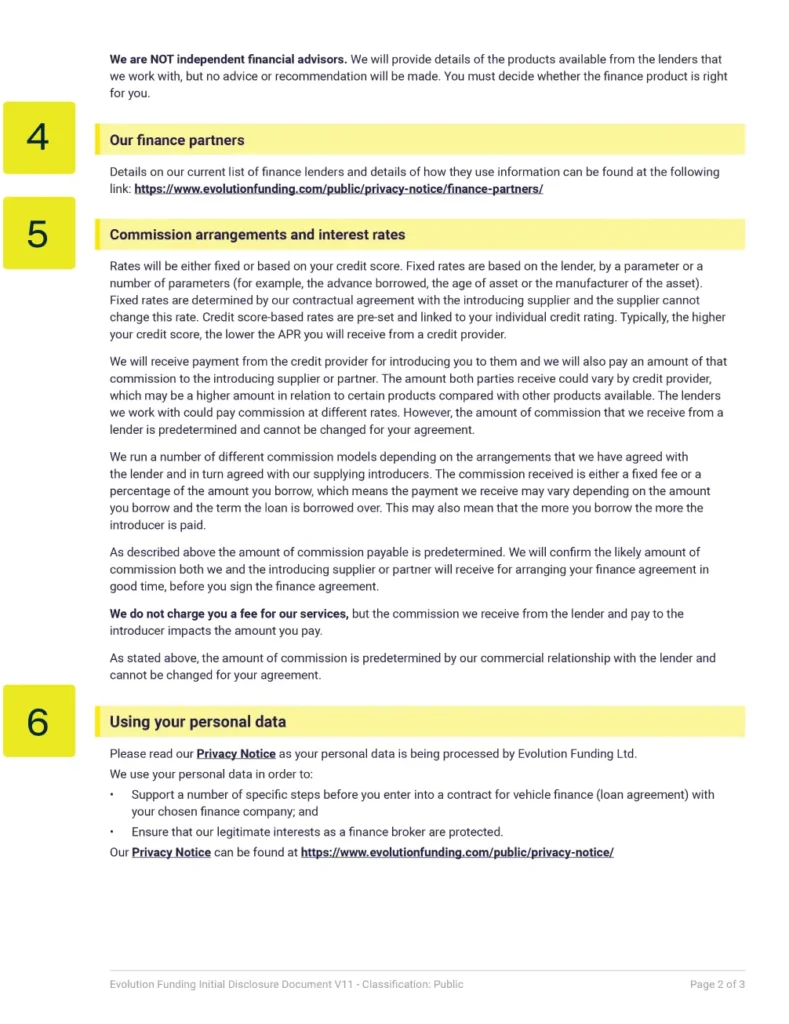

4. Our finance partners

- Details of the finance partners you work with and where customers can find more information on how they use personal data.

5. Commission arrangements and interest rates

You must include details on the existence, nature and amount of all your commission arrangements, and if they impact on your impartiality in recommending a product to a customer, which in turn may affect the customer’s willingness to transact. Clear commission disclosure is essential for meeting your responsibilities and promoting customer understanding.

You should consider including the following details:

- What types of commission you receive – this can be in broad terms.

- How the commission can differ between credit provider, product and other factors e.g. amount of the loan, term etc.

- If the customer is eligible for two or more products and your commission varies, you need to disclose this.

- If the amount of commission you receive is pre-determined, and if it can be changed for the customer’s agreement.

- Informing the customer that they will be provided details of the amount of commission, and when e.g. in good time before signing their agreement.

- If you receive other types of support, such as unit stocking, marketing or training from a lender, that may influence your decision when placing business.

- The types of rates you can offer customers and explain how these are set (in general terms).

- What, if any, parameters could change the rate the customer is offered, e.g. credit score, age of vehicle, loan amount.

- Whether you charge the customer any fees for your services.

- If the commission received impacts on the amount the customer pays (i.e. if your contractual APR enables your provider to pay you commission) for example, “the commission we receive from the lender/broker impacts the amount you pay”.

6. Using your personal data

- How customers’ personal data will be used.

- Where customers can find your privacy notice.

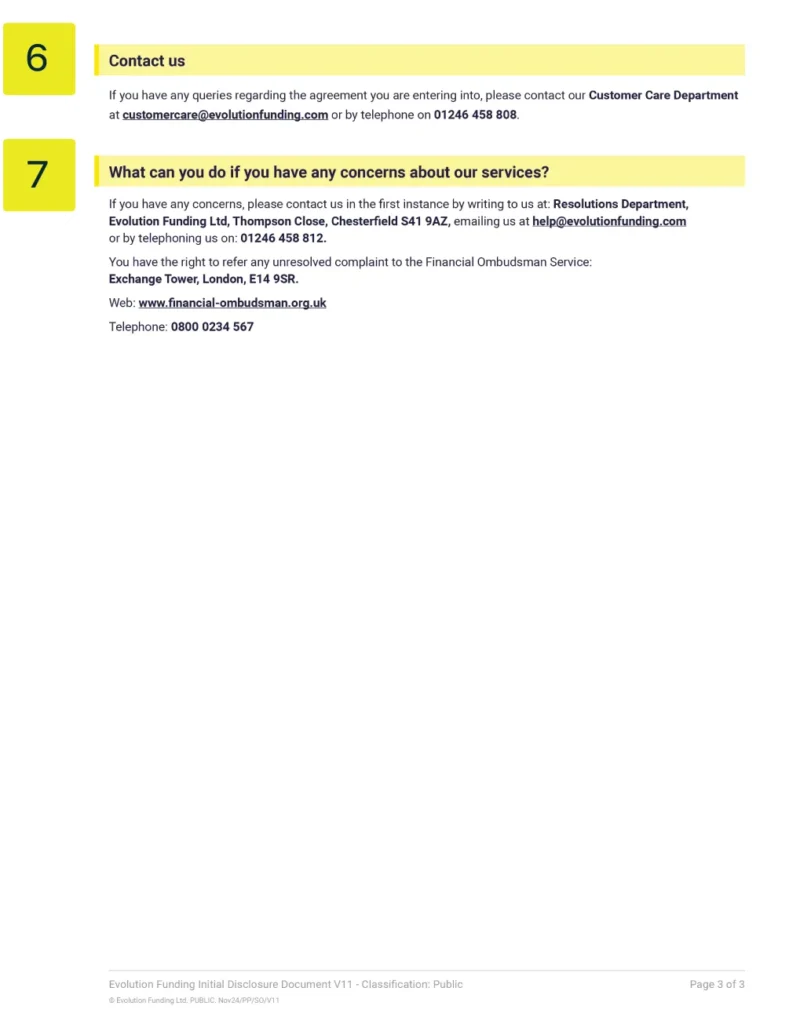

7. Contact us

- Provide details of how customers can contact you if they have a question.

8. Complaints

- You must provide details of how customers can contact you if they wish to make a complaint.

- You must also explain that the customer has the right to refer any unresolved complaint to the Financial Ombudsman Service and provide their contact details:

- Postal address: Financial Ombudsman Service, Exchange Tower, London, E14 9SR.

- Web: www.financial-ombudsman.org.uk

- Telephone: 0800 0234 567

What to do with your IDD

When you deal with Evolution, we will also be discharging our regulatory duties and ensuring our compliance with law and regulation. Evolution will share our IDD with the customer to explain our role in the transaction. We will also obtain the customers fully informed consent to the commission payable from the lender to Evolution and from Evolution to you, in good time ahead of the customer signing the lenders documentation.

To meet your legal and regulatory obligations, you should:

1. Share your IDD at Key Stages of the Sales Process

- Provide your IDD early in the customer journey, ideally before any finance discussions. This gives customers a chance to review commission information in advance of any decision being made.

- At this stage you may not know the exact commission amount that you will receive, but you should clearly inform the customer that you will earn a commission and explain how this will be calculated, to the fullest extent you can, including via your IDD as early as possible in the process.

- Consider sharing the IDD at several points in the sales process, such as in sales emails, and in initial discussions, to ensure customers are informed early and regularly

2. Document the IDD, Commission Disclosures and Customer Acknowledgements

- Keep records of when and how the IDD and any information around commission was provided to the customer. This helps you check your processes are working effectively and act as evidence of regulatory and legal compliance if you need them.

- Whenever possible, which may include at multiple points in the customer journey, obtain customer acknowledgment of the commission disclosure, either in writing or through recorded confirmations.

- We will obtain fully informed written consent from the customer for the commission payable to Evolution and you. This will be time and date stamped in Evolution’s systems, providing a full and auditable record of the customer giving fully informed consent.